The CLARITY Act has stalled in Senate Banking deliberations, setting back an array of market rules that would solidify into law most of the pro-crypto stance that took hold in the President Donald Trump administration.

Yet, Congress may have handed crypto markets an unexpected experiment. Galaxy Research puts the odds of enactment this year at roughly 50-50, possibly lower, with unresolved disputes over DeFi provisions, jurisdiction, and stablecoin yield language.

The bill spans token classification, exchange and broker-dealer registration, software carveouts, and DeFi provisions, with the rewards dispute representing one contested layer inside a much larger framework.

On the rewards layer is where Wall Street’s most concrete stablecoin-related fear lives, and a stall could let the market answer it before Congress does.

The rewards lane

The GENIUS Act explicitly bars stablecoin issuers from paying interest or yield solely for holding a payment stablecoin, resolving the simplest version of the fight.

The harder question is if exchanges and third parties can offer cash back, referral bonuses, or promotional yields without running into the same prohibition.

Both the OCC’s March proposal and the FDIC’s April proposal extended anti-evasion presumptions to some affiliate and related third-party arrangements, narrowing the lane.

Yet, both documents are still proposed rules pending finalization, and regulators are still defining the practical scope of what counts as prohibited.

Banks have framed this open perimeter as an existential threat to their competitiveness. The ABA’s community bank letter cited up to $6.6 trillion in deposits as potentially at risk, warning that exchange-funded inducements could pull savings out of the banking system.

Standard Chartered put a more bounded forecast of up to $500 billion in deposit outflows to stablecoins by the end of 2028, with regional banks carrying the most exposure.

The argument centers on exchange-funded rewards that make stablecoin balances functionally competitive with bank deposits while avoiding the reserve requirements, capital rules, and insurance costs that banks bear.

The White House Council of Economic Advisers published a direct rebuttal in April, finding that eliminating stablecoin yield would increase bank lending by about $2.1 billion, or roughly 0.02%, and impose an $800 million net welfare cost.

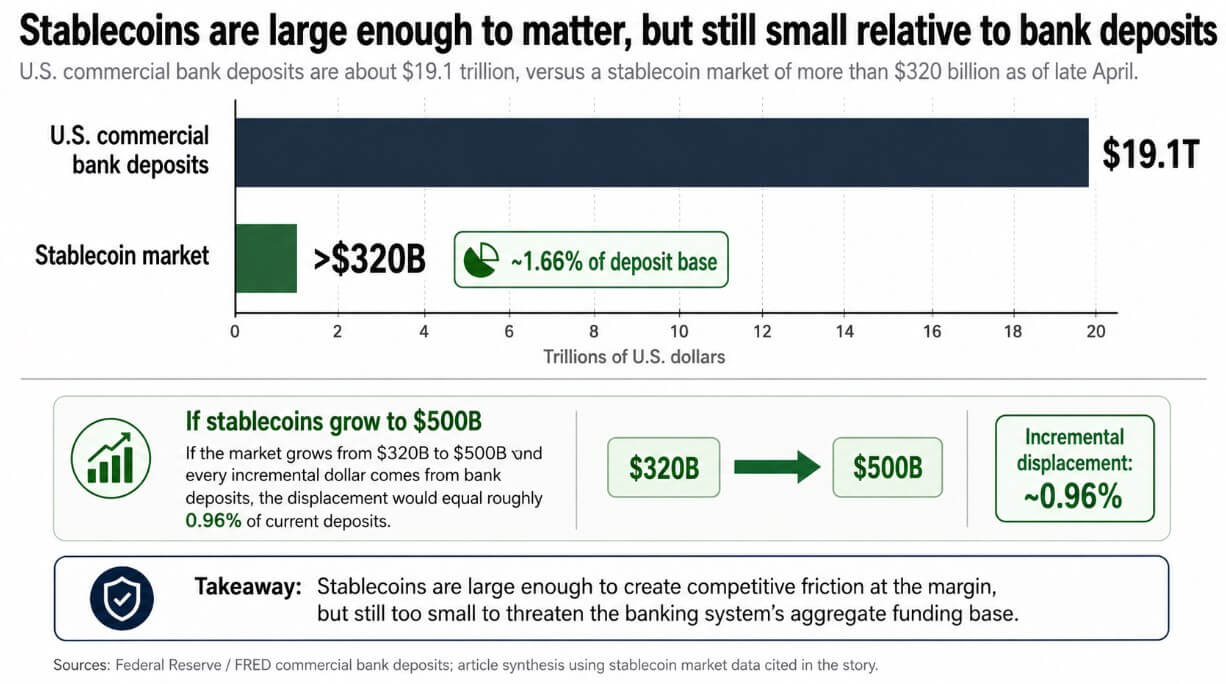

The stablecoin market stood at over $320 billion as of Apr. 27, against roughly $19.1 trillion in US commercial bank deposits.

At about 1.66% of the deposit base, stablecoins are large enough to generate competitive friction at the margins and small enough for the system’s aggregate funding to hold.

If the stablecoin market grew from $320 billion to $500 billion and every incremental dollar came from bank deposits, the displacement would be roughly 0.96% of current deposits. The amount is enough to test community institutions’ pricing power while leaving the system’s aggregate funding intact.

The positive outcome

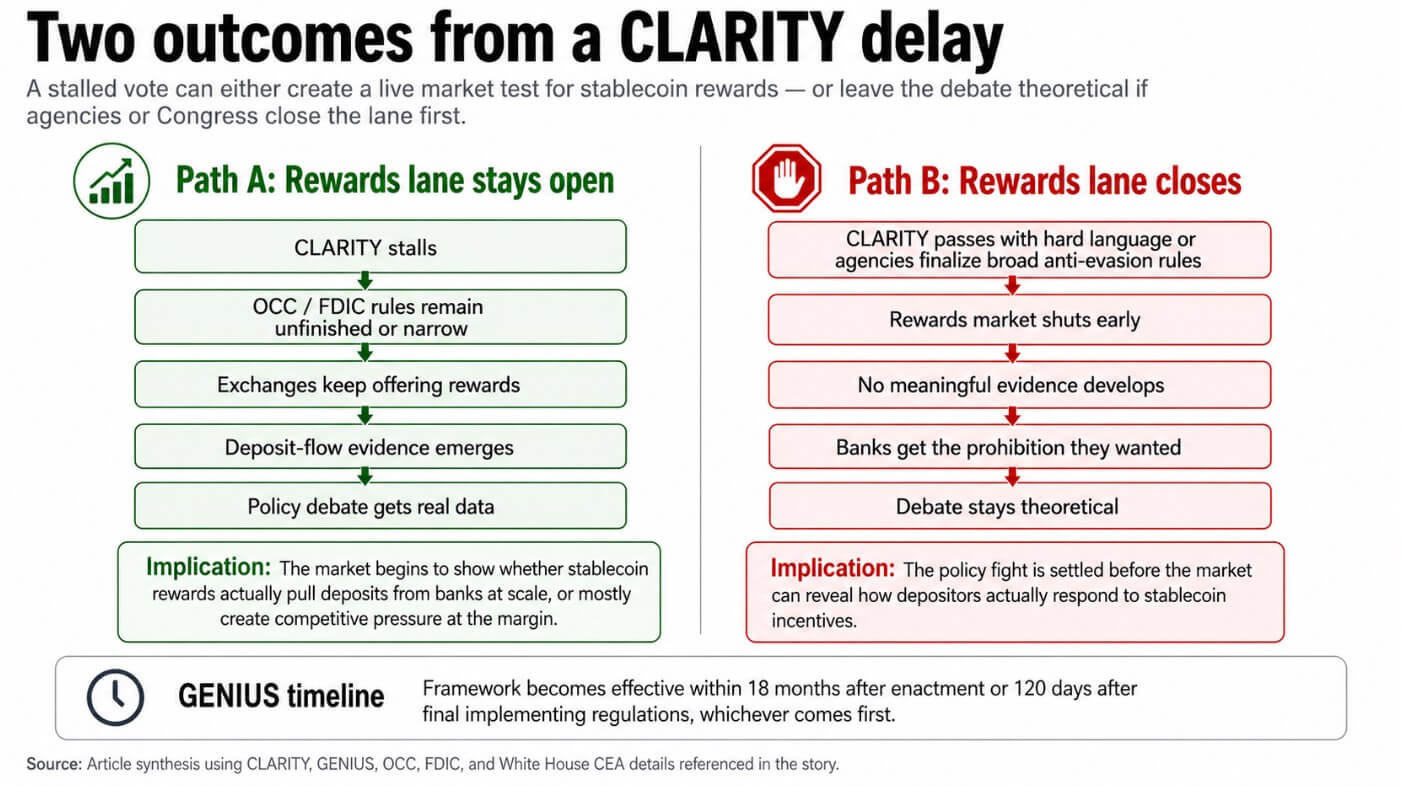

If CLARITY stalls and agency rulemaking does not close the rewards lane, exchanges can keep operating in the unsettled perimeter.

In that environment, the rewards market runs long enough to generate observable data, such as flows between bank accounts and on-chain balances, moves in retail cash allocation, and competitive responses from banks on deposit rates.

Congressional hearings have spent eighteen months generating arguments, and a legislative delay could generate evidence. The difference between the ABA’s $6.6 trillion alarm and the CEA’s $2.1 billion lending effect would begin to fill in with actual data.

The global dimension makes any data that emerges immediately relevant beyond US borders.

MiCA explicitly bars issuers of e-money tokens from paying interest and extends that restriction to crypto-asset service providers. Hong Kong runs a license-based stablecoin-issuer regime.

The BIS noted in April that the main cross-jurisdiction split now centers on whether exchanges and CASPs may offer rewards, with some markets prohibiting them, others restricting retail access, and others leaving no explicit ban.

A BIS working paper published in February found that a $3.5 billion five-day inflow of stablecoins lowers 3-month T-bill yields by 2.5 to 3.5 basis points, providing evidence that stablecoins already connect to the front end of the Treasury curve in measurable ways.

If the US gray area produces deposit-flow data, it becomes the first empirical input into an international policy debate that has run entirely on projections.

| Claim / source | What they argue | Magnitude cited | What a live market test would show |

|---|---|---|---|

| ABA / banks | Rewards could drain deposits from banks | Up to $6.6T at risk | Whether deposit outflows actually appear at scale |

| Standard Chartered | Stablecoins could pull meaningful deposits by 2028 | Up to $500B | Which banks are most exposed, especially regionals |

| White House CEA | Banning yield has limited bank-lending upside | $2.1B lending effect; ~0.02% | Whether actual rewards change deposit behavior more than the model suggests |

| Market reality | Stablecoins already exceed $320B | ~1.66% of deposit base | Whether competition shows up in rates, flows, and retail cash allocation |

A bearish outcome

Congress or agencies could close the lane before the test generates anything useful.

If the OCC and FDIC finalize anti-evasion rules broadly enough to reach promotional and activity-linked rewards, or if CLARITY passes with hard yield-prohibition language, the experiment ends before it starts.

Banks get the prohibition they sought, the CEA’s small-number estimate becomes the only available empirical reference point, and the debate moves forward on the same contested theoretical ground.

The White House CEA’s April paper noted that the GENIUS framework becomes effective within 18 months after becoming law, or 120 days past final implementing regulations, whichever comes first. This clock limits how long any gray area can run, regardless of what Congress does with CLARITY.

The delay carries structural costs that compound regardless of what the stablecoin rewards market reveals, such as token classification staying ambiguous, software developers carrying liability risk, DeFi protocols operating under contested regulatory authority, and exchange and broker-dealer registration frameworks sitting in limbo.

Those costs fall on the industry and its users the longer the bill stays idle.

Deposits leaving banks for stablecoin rewards would flow toward reserve assets such as T-bills and repo, redirecting funding from bank balance sheets to the front end of the Treasury curve.

The test reveals if rewards reshape deposit behavior at the margins, and for which depositors.

At the current stablecoin market size, that is a deposit sensitivity check, a real-world measure of bank pricing power and competitive friction that the industry, at this scale, has only modeled.

A CLARITY stall means watching that mechanism either accelerate deposit migration or hold it steady despite every competitive incentive, and either result produces the first real deposit-behavior data a market this size has ever generated.